Kdo má nárok na stravenky

Nárok na stravenku

Většina zaměstnavatelů má nastaveno, že nárok zaměstnance na stravenku vzniká za každý den na pracovišti, a většinou kopíruje možnost daňového odpočtu. Zaměstnanec tedy musí v rámci směny odpracovat alespoň 3 hodiny. Podmínky pro nárok na stravenky jsou plně v kompetenci zaměstnavatele.

Archiv

Jak na Stravenkový paušál

Zaměstnavatel si může uplatnit jako daňově uznatelný náklad až 55 procent ceny jídla nebo stravenky. Zbylých 45 procent doplácí zaměstnanec ze své čisté mzdy. Na stravenku v hodnotě 100 korun tak zaměstnavatel přispívá 55 korun, které zaplatí stravenkové firmě a odečte si tento náklad z daňového základu.

Jak nastavit Stravenkový paušál v pohodě

Program POHODA automaticky počítá pro celý srpen s osvobozeným limitem 82,60 Kč. V případě, že poskytujete svým zaměstnancům paušál nad uvedený limit, je nutné ve mzdách za srpen upravit (snížit) částku, kterou program vypočte v poli „z toho nad limit“ v části Stravenkový paušál na záložce Čistá mzda.

Jak zaúčtovat Stravenkový paušál nad limit

Jak účtujeme stravenky

Pokud se zaměstnavatel podílí na úhradě nad hranici 55 %, musí tuto část zaúčtovat na účet 528 – Ostatní sociální náklady, protože se jedná o náklad daňově neuznatelný. Zbývající část placenou zaměstnancem se pak zaúčtuje na vrub účtu („MÁ DÁTI“) 335 – Pohledávky za zaměstnanci.

Kdy není nárok na Stravenkový paušál

U směn, které jsou delší než 11 hodin, není možné poskytnout paušál tak, aby byl daňově zvýhodněný jako stravenky. Osvobození na straně zaměstnance platí pouze pro jednu směnu.

Kdy vzniká nárok na diety

Při služební (pracovní) cestě, máte nárok na stravné (diety). Ty se poskytují, pokud je pracovní cesta delší než 5 hodin. U zahraniční služební cesty, to musí být více než 1 hodinu mimo ČR. Stravné (diety) jsou nezdanitelný příjem (neplatí se daň, sociální a zdravotní pojištění).

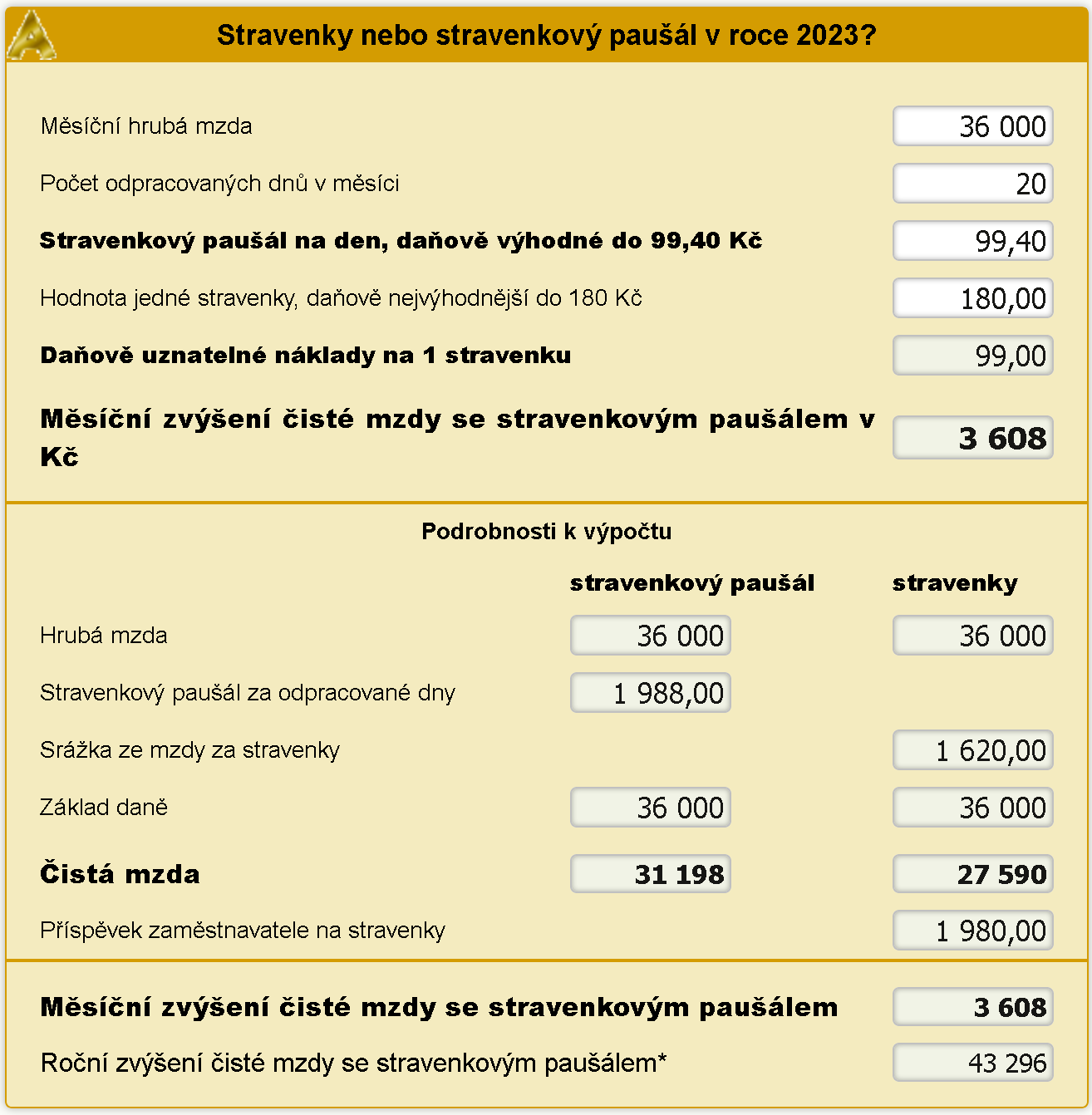

Co je výhodnější stravenky nebo paušál

Kdy se vyplatí stravenkový paušál

Částka nad tento limit totiž podléhá 59,8 % zátěži (33,8 % odvody pojistného zaměstnavatele za zaměstnance, 11 % odvody pojistného zaměstnance, 15 % sazba daně z příjmů ze závislé činnosti), kdežto v případě poskytnutí stravenky pouze 19 %, resp. 15% zátěži.

Co je výhodnější Stravenkový paušál nebo stravenky

Výhodou stravenek je, že u zaměstnance jsou osvobozeny bez limitu, pro zaměstnavatele je to daňový náklad do limitu, stravenkový paušál je naopak u zaměstnance osvobozen do limitu, u zaměstnavatele daňový náklad bez limitu, což je pro něj výhodnější.

Co je Stravenkový paušál 2023

horní limit stravného při pracovní cestě trvající 5 až 12 hodin 153 Kč, takže v roce 2023 je u zaměstnance osvobozen od daně z příjmů peněžitý příspěvek zaměstnavatele na stravování (stravenkový paušál) až do výše 70 % z částky 153 Kč za jednu směnu, tedy 107,10 Kč.

Jak se Vypocita Stravne

Kolik je stravné v roce 2022 při služební cestě v ČRDélka služební cesty 5 až 12 hodin = 99 Kč až 118 KčDélka služební cesty 12 až 18 hodin = 151 Kč až 182 KčDélka služební cesty nad 18 hodin = 237 Kč až 283 Kč

Jak se bude účtovat Stravenkový paušál

Jak stravenkový paušál účtovat Je-li peněžitý příspěvek vyplácen společně se mzdou, účtujeme standardně na 527/331. V ostatních případech můžeme použít 527/333.

Jak spočítat cestovní náhrady 2023

Výpočet cestovních náhrad 2023základní náhrada = 100 (km) * 5,2 (sazba základní náhrady pro osobní vozidla) = 520 Kčnáhrada za pohonné hmoty = 5 (spotřeba auta v litrech na 100 km) * 44,10 (cena nafty) = 220,5 Kčcelková cestovní náhrada = 520 + 220,5 = 740,5 Kč

Kdy má řidič nárok na diety

Při služební (pracovní) cestě, máte nárok na stravné (diety). Ty se poskytují, pokud je pracovní cesta delší než 5 hodin. U zahraniční služební cesty, to musí být více než 1 hodinu mimo ČR. Stravné (diety) jsou nezdanitelný příjem (neplatí se daň, sociální a zdravotní pojištění).

Na co mám nárok při pracovní cestě

Za každý kalendářní den pracovní cesty poskytne zaměstnavatel zaměstnanci v nepodnikatelské sféře stravné ve výši: 129 až 153 Kč, trvá-li pracovní cesta 5 až 12 hodin. 196 až 236 Kč, trvá-li pracovní cesta déle než 12 hodin, nejdéle však 18 hodin. 307 až 367 Kč, trvá-li pracovní cesta déle než 18 hodin.

Kdy vznika narok na Cestak

Za každý kalendářní den pracovní cesty poskytne zaměstnavatel zaměstnanci v podnikatelské sféře stravné nejméně ve výši: 129 Kč, trvá-li pracovní cesta 5 až 12 hodin. 196 Kč, trvá-li pracovní cesta déle než 12 hodin, nejdéle však 18 hodin. 307 Kč, trvá-li pracovní cesta déle než 18 hodin.

Kdo má nárok na diety

Při služební (pracovní) cestě, máte nárok na stravné (diety). Ty se poskytují, pokud je pracovní cesta delší než 5 hodin. U zahraniční služební cesty, to musí být více než 1 hodinu mimo ČR. Stravné (diety) jsou nezdanitelný příjem (neplatí se daň, sociální a zdravotní pojištění).